Vi

Vi

En

En

简体中文

简体中文

日本語

日本語

'%2F><path%20id%3D'Path_249'%20data-name%3D'Path%20249'%20class%3D'cls-1'%20d%3D'M109.655%2C40h-12.9c-.417%2C0-.759.225-.759.5s.341.5.759.5h12.9c.417%2C0%2C.759-.225.759-.5S110.072%2C40%2C109.655%2C40Z'%20transform%3D'translate(-90.407%20-36.388)'%2F><path%20id%3D'Path_250'%20data-name%3D'Path%20250'%20class%3D'cls-1'%20d%3D'M55.836%2C72h-15.2a.514.514%2C0%2C1%2C0%2C0%2C1h15.2a.514.514%2C0%2C1%2C0%2C0-1Z'%20transform%3D'translate(-36.207%20-65.498)'%2F><path%20id%3D'Path_251'%20data-name%3D'Path%20251'%20class%3D'cls-1'%20d%3D'M211.034%2C104h-2.276c-.417%2C0-.759.225-.759.5s.341.5.759.5h2.276c.417%2C0%2C.759-.225.759-.5S211.452%2C104%2C211.034%2C104Z'%20transform%3D'translate(-191.648%20-94.608)'%2F><path%20id%3D'Path_252'%20data-name%3D'Path%20252'%20class%3D'cls-1'%20d%3D'M40.759%2C105h12.9c.417%2C0%2C.759-.225.759-.5s-.341-.5-.759-.5h-12.9c-.417%2C0-.759.225-.759.5S40.341%2C105%2C40.759%2C105Z'%20transform%3D'translate(-35.952%20-94.608)'%2F><path%20id%3D'Path_253'%20data-name%3D'Path%20253'%20class%3D'cls-1'%20d%3D'M55.836%2C136h-15.2a.536.536%2C0%2C1%2C0%2C0%2C1.055h15.2a.536.536%2C0%2C1%2C0%2C0-1.055Z'%20transform%3D'translate(-36.207%20-123.279)'%2F><%2Fsvg>)

Knowledge

1. What is derivatives? Derivatives are financial instruments whose values are based on an agreed-upon underlying assets. Common derivatives include: Forwards:

Đấu giá mới nhất

During a trading day, profits/losses will fluactuate with real-time market price (mark – to – market)

At the end of a trading day, all profits/losses of closed and open positions are realized and paid to investors.

For open positions, VSD will calculate profits/losses as followings:

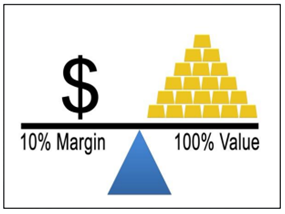

Leverage refers to using little amount of outlay to control large positions in derivatives trading.

For example, investor A decides to BUY 10 index futures contracts at price 700 and maturity date December 2017:

|

Contract code |

Quantity |

Executed price |

Multiplier |

|

VN30F1712 |

10 (LONG) |

700 |

100,000 |

|

If initial margin rate is 10%:

If initial margin rate is 15%:

|

|

|

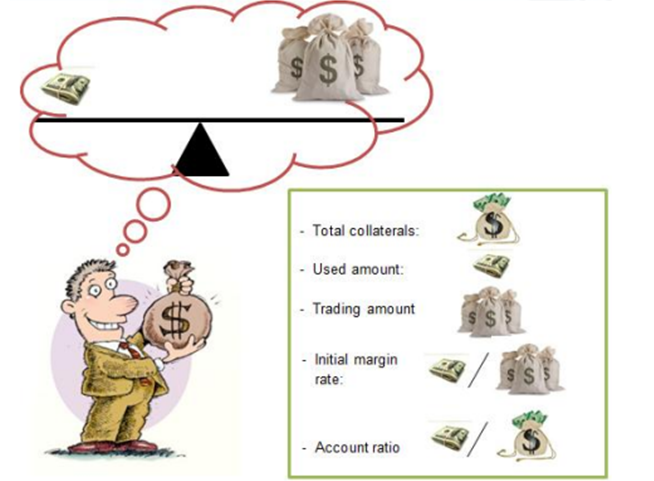

Initial margin refers to the minimum collateral values that investors must have to trade a specific derivatives contract. Initial margin rate can be used to calculate leverage effect of the contract. Account ratio is the proportion of collaterals used for derivatives trading. Investors can use this figure to calculate the remaining values of collateral assets for next transactions. |

|

Account ratio = Margin Requirements / Total Eligible Collateral amount

In which:

Margin requirements = IM + VM + SM + DM

Total Eligible Collateral amount = Cash + Eligible securities

Account ratio will vary real-time with market prices of derivatives contracts

For example:

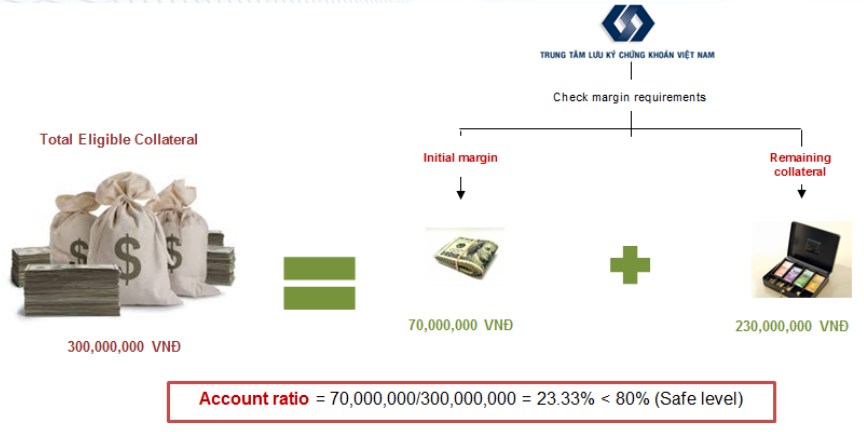

Step 1. An investor deposits 240 million VND in cash and 100 million VND in stock as collaterals for derivatives trading.

To ensure the minimum proportion of cash collateral is 80%, Total Eligible Collateral will be: 240 million + min (100 million; 25% * 240 million) = 300 million VND

Step 2. The investor expects the market will go “up”, thus he decides to BUY index futures contracts matured at December 2017

|

Contract code |

Quantity |

Executed price |

Multiplier |

IM rate |

|

VN30F1712 |

10 (LONG) |

700 |

100,000 |

10% |

Step 3. VSD checks Initial margin requirment of the transaction

|

Contract code |

Initial margin |

Margin requirements |

Total eligible collateral |

|

VN30F1712 |

10 * 700 * 100,000 * 10% = 70,000,000 VND |

70,000,000 VND (Initially, VM = 0) |

300,000,000 VND |

Step 4. VSD checks Account ratio of the trading account

|

|

Stocks |

Futures |

|

First trading day |

The first day listed in stock exchange |

- The first day listed in stock exchange - The number of listed contracts does not vary: new contracts will be automatically listed after a contract is matured |

|

Listing volume |

Limited by issuing amounts of stocks |

Unlimited |

|

Number of contract codes |

Each stock code is corresponding to an individual stock/bond/fund certificate |

Each contract has different codes corresponding to contract months |

|

Short-sell |

Not allow to short sell |

Allow to short sell |

|

Final trading day |

The day before that stocks are unlisted |

The final day that futures contracts have value |

|

Payment period |

T+3 |

Daily settlement |

|

Payment method |

Physical delivery |

Cash settlement and physical delivery |

|

Payment mechanism |

Exchange stocks and cash |

Central Counterparties (CCP) |

|

Margin |

Not compulsory (a facility that brokerage firms provide to customers) |

Compulsory to ensure payment ability |

|

Subjects of margin |

Buyers |

Buyers and sellers |